The Third Pillar: Why Energy Is the Undervalued Core of the AI Revolution

When NVIDIA CEO Jensen Huang told the Financial Times that “China is going to win the AI race,” he wasn’t talking about algorithms or GPUs. He was talking about energy — about a nation that can power its ambitions more cheaply and more freely than its rivals.

That quote landed like a thunderclap in the investment world because it reframed what the AI race really is: not a competition of code or chips, but a race for electrical dominance.

The Three Pillars of AI Supremacy

Every dollar flowing into artificial intelligence rests on three interlocking foundations:

- Code – The software and model ecosystems that define intelligence.

- Chips – The silicon that performs it.

- Energy – The power that enables both to function.

The first two have already been bid to the stratosphere. The third has not — and that disconnect is about to define the next decade of capital markets.

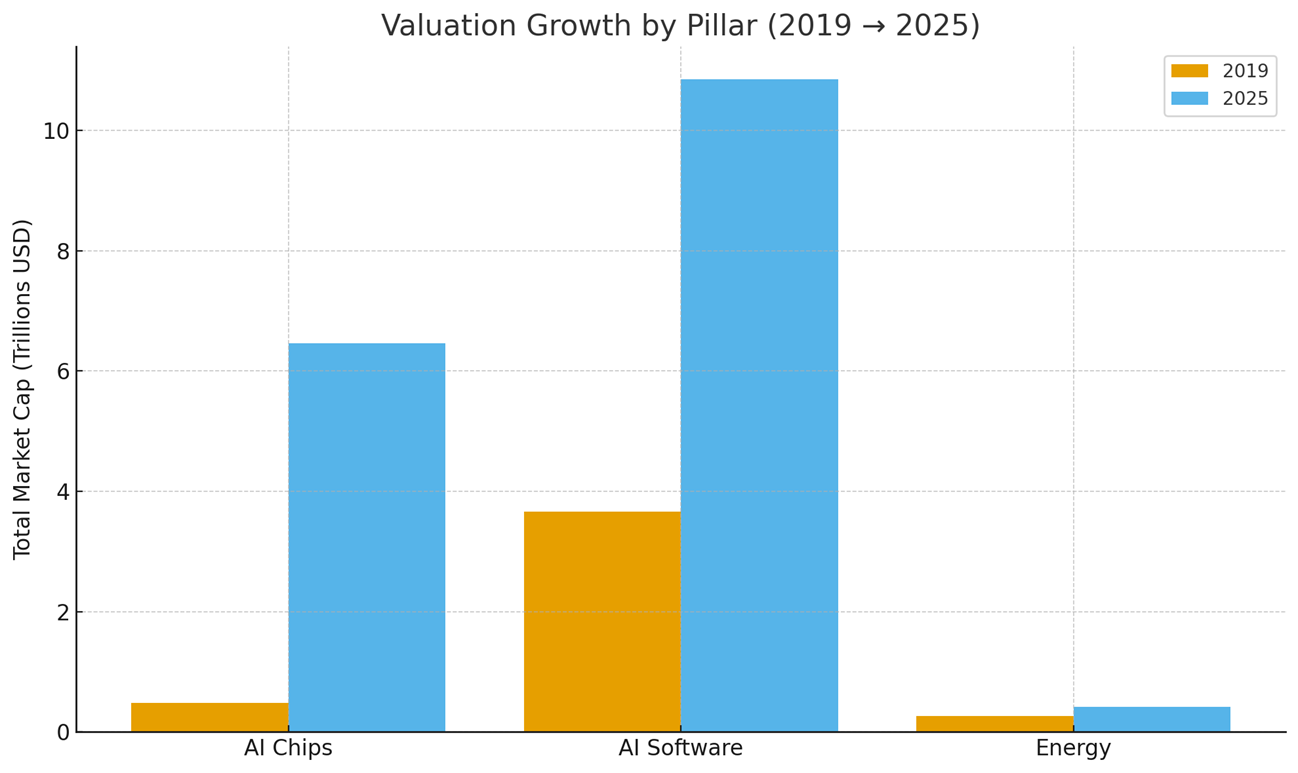

A Six-Year Story of Imbalance

| Pillar | Representative Leaders | 2019 Aggregate Value (USD Tr) | 2025 Aggregate Value (USD Tr) | Growth % (2019→2025) |

| Code (AI Software) | Microsoft • Alphabet • Amazon • Meta | 3.66 | 10.85 | +196 % |

| Chips (AI Hardware) | NVIDIA • AMD • TSMC | 0.48 | 6.47 | +1 248 % |

| Energy / Utilities | NextEra • Duke • Southern • Exelon | 0.26 | 0.41 | +57 % |

(Market-cap data 2019 → Nov 2025; compiled from SEC filings and financial databases.)

In six years, chipmakers increased their market value over twelve-fold, software firms tripled, and energy barely moved. Yet every one of those chips and cloud instances runs on the same limited grid.

This is the greatest mispricing of the century: the world has valued intelligence but forgotten power.

The Real Bottleneck

Data centers are now the fastest-growing industrial electricity load in the United States.

The Department of Energy warns of capacity shortfalls and “imminent blackout risk.” Energy Secretary Chris Wright has stated bluntly that “the grid is reaching its limit.”

Meanwhile, China is adding low-cost generation and subsidizing power for AI manufacturing. Huang’s observation was unambiguous: in China, “power is free.”

If the U.S. cannot scale and control its energy resources, its advantage in software and chips will collapse under its own consumption.

Already in an emergency

- At least three major emergency orders in 2025: May, July, October (plus multiple extensions).

- These emergency orders address generation unit retirements, grid-capacity shortfalls and extreme demand (summer & winter).

- They deployed DOE’s Section 202(c) authority to force online or extend operation of generation units to avoid blackout risk.

- The frequency and geographical spread (Midwest, Mid-Atlantic, multi-state region) indicate the DOE views grid reliability as an ongoing, not isolated, emergency

- DOE and National Grid operators first shortfalls below reserve margins are in the winter months – making Powder Watts FlexiWatt a priority solution.

Critical unavailability of energy leads to Hyperscalers filing formal complaints against electric utility companies:

The tension between skyrocketing AI power demand and limited grid capacity is no longer just forecast. Grid operators have been delaying grid hookups for several years now. Additionally, in late 2025, Bloomberg reported that Amazon filed a formal complaint against PacifiCorp—the Berkshire Hathaway–owned utility serving much of the Pacific Northwest—after the company was unable to supply sufficient electricity for four planned data-center campuses in Oregon. According to Amazon’s filing with state regulators, PacifiCorp delivered too little power to one site, “no power” to a second, and “refused to even complete its own standard contracting process” for the third and fourth. The utility, citing the need to protect “customer affordability,” responded that it was “open to ongoing discussions with Amazon to reach a resolution that achieves balanced outcomes for all customers.” The dispute underscores the growing strain between hyperscalers racing to deploy AI infrastructure and utilities struggling to maintain reliability and equity on an already overextended grid.

Where Smart Capital Is Headed Next

The investment logic is now shifting:

- Software has achieved full valuation saturation.

- Chips are at speculative multiples that assume infinite compute demand.

- Energy, the enabling constraint, still trades at utility-era valuations — low growth, low excitement, low multiples — even as it becomes the gating factor for every AI deployment – and as NVIDIA’s Jensen Huang states – the lynchpin to which Nation wins the AI supremacy race.

This is a once-in-a-generation asymmetry. When markets finally price energy as the scarce input to intelligence, the re-rating will be explosive.

Powder Watts: Converting Waste into Capacity

Into this gap steps Powder Watts, a company that embodies what modern energy should look like: clean, software-defined, and immediately scalable.

Across North America, more than 20 million buildings use rooftop heat cables to melt ice — devices that typically run 24 hours a day, all winter. They consume an estimated 140 TWh of electricity each year — roughly half the output of all U.S. solar generation in 2024.

Powder Watts’ patented computer-vision and weather-integrated control system converts these always-on circuits into a NSF and DOE endorsed flexible, dispatchable virtual power plant, cutting energy consumption by 70–90 %. It creates massive immediate VPP DER grid capacity with Shape, Shift and Shed – liberating existing power back to the grid.

A Financing Model Built for Scale

For investors, the economics are exceptional:

- Utilities fund roughly 70 cents of every dollar required for installation through rebates and virtual-power-plant incentive programs.

- Powder Watts earns recurring SaaS and performance payments for energy returned to the grid — a structure similar to a PPA, but without fuel, permitting delays, or exposure to commodity prices.

- The result: each investor dollar is leveraged threefold by utility capital while generating long-term revenue streams.

- No permitting, zoning, NEPA, or grid intertie delays.

That alignment between public-sector energy security and private-sector return is rare — and it’s precisely what accelerates deployment.

Why Energy Is the Next Tech Boom

The first trillion-dollar winners of the AI era built the digital mind.

The next will secure its metabolism — the energy flows that enable growth and keep it alive.

Powder Watts illustrates what that future looks like:

- Patented control of a 140 TWh unregulated load,

- Rapid scalability driven by 70 % utility funded deployment,

- Tech-style recurring revenue in a critical infrastructure sector,

- And direct alignment with national-security and climate mandates.

Closing Thoughts

The AI race isn’t just about smarter algorithms or faster silicon.

It’s about who can actually make them happen and power them.

Software and chips may have defined the first half of this decade.

Energy will define the next.

As investors finally recognize that every line of code and every GPU is worthless without electrons, they’ll look for companies that create energy capacity where none existed — efficiently, immediately, and profitably.

That’s what Powder Watts delivers.

And in the coming repricing of the energy pillar, it represents something rarer than a good story — a generational opportunity.

For contact:

Investor@powderwatts.com